Running a Budget Surplus Consistently

Cars: The Monkey On Your Budget Back

Dealing With the Budget Problem

The Magic Secrets of Personal Finance

What To Do When You Get Down To Just Rent and Car Payments

Dealing With Money Conflict In Marriage

Should You Pay Cash for a Car?

Note: some aspects of this concerning interest rates were written in 2003 and 2004, when interest rates were very different. The principles remain the same.

Updated 11/29/2016 reflective of what I have learned in the last decade or so. New material is in bold

Even before I had some minor success with a couple of startups, I had moved from just below the poverty line to reasonable comfort, with a house, a year's expenses in savings, and no debt (other than a house mortgage). I've learned a few things, some in classes, some in the college of hard knocks. I've also had a little help along the way from relatives, some of it purely one-sided, and some of it mutually beneficial. I would like to pass on this information to those of you who are just getting started in life. (Some of this advice will be valuable to those of you who aren't just getting started in life, too.)

The most valuable three hours I think I have ever spent was at a free financial planning class in Irvine in 1985. It was, quite literally, free. Yes, they were trying to sell us on paying for a more comprehensive class, but what I learned in those three hours, in retrospect, was worth $10,000 to me. What I learned there was freely given, and I give it to you freely as well.

“My other piece of advice, Copperfield,” said Mr. Micawber, “you know. Annual income twenty pounds, annual expenditure nineteen nineteen six, result happiness. Annual income twenty pounds, annual expenditure twenty pounds ought and six, result misery." [Charles Dickens, David Copperfield, ch. 12]

To translate it into modern terms: "Take home $40,000 a year, and spend $39,500, result happiness. Take home $40,000 a year, and spend $40,500, result misery." Obviously, the greater the difference--either way--the more rapidly you will see the result.

At one time, I commuted 25 miles each way to work. Because only part of the costs of commuting are visible on a daily or weekly basis, I didn't realize that I was spending more than I was earning. When the invisible part of the commuting costs would show up, in a brake job, tune-up, or tires, it was always a crisis--and of course, charging those bills just led to the next crisis--interest on credit cards (to be discussed later).

You must figure out what you are actually spending. You will not find this out by adding up your bills for a month. There are too many big bills that only come up every few months (tune-up, brake job, paying for that vacation you just took). Proper budgeting means going through your check register for many months. It also means having a realistic picture of what you are buying in cash. My experience is that most people, especially most people without kids, are absolutely shocked by how much they spend in cash eating out each month. Start saving the receipts, even if it's just a Big Mac, fries, and a Coke--add them up at the end of the month.

Are you increasing your credit card debt every month? That increase in debt--the amount that your balance increases in month--is part of your monthly expenditures. Don't tell yourself, "This was a one-time expense--it won't happen again." There are very, very few such expenses.

For most people, there is one additional expense that is hard to measure, and that's car repairs and maintenance. The cents per mile figure that the federal government allows for tax purposes really doesn't do the job adequately. The major marginal maintenance expenses of operating a car are usually gasoline, tires, brakes, oil changes, and tune-ups. You know (or should know) roughly what sort of gas mileage you get: 20 miles per gallon is 1/20 gallons per mile. Multiply by the price of gas, then multiply by the number of miles a month that you drive. Find your last tire purchase receipt, divide the total price tag by the number of miles you get on that set of tires (e.g., $300 for four tires, they lasted 30,000 miles, that's $.01 per mile). Ditto for brakes, oil changes, and tune-ups. Don't worry if you don't have the exact amount, or the exact number of miles--it will be close enough.

Insurance and registration fees are primarily determined by the number of months that you have the car--not the number of miles you drive. Some auto insurers will determine rates by your daily commute, and for what purpose you use the car--but this usually doesn't make a big difference in the total bill. Treat auto insurance as a monthly expense, and don't try to factor it into your mileage costs.

Depreciation is often the biggest chunk of the expense of driving a car, but unless you buy new cars and then sell them every three or four years, this is not likely to be a significant part of your annual budget--and you do have the advantage that you don't suffer the depreciation until you actually sell the car. This isn't really a regular expense for you. Here's a tip: buy cars that are still under factory warranty, but are 1-2 years old. In 2002 I bought a 2000 Corvette with 23,000 miles on it for $33,500. Brand new, it cost about $48,000. The first buyer thus spent 63 cents a mile JUST ON DEPRECIATION! I would have to drive the car another 60,000 miles to knock another $14,500 off its value. I eventually sold it with 107,000 miles for $8500.

The one uncertainty is repairs. While piling up debt by buying a new car is usually a mistake, there are circumstances where it can make sense. What do you get with a new car (or, in most cases, a slightly used car)? The remainder of the factory new car warranty. Relatively new cars are also eligible for extended warranties. If your car with 90,000 miles on it has already demanded a transmission rebuild, a valve job, and a new master cylinder--and you have no idea what it will need next--it might make sense to buy a new, cheap, sensible car. You will have a regular monthly car payment, but you can budget around that, in a way that you can't budget around the next repair that your heap needs (or that the mechanic claims that it needs). "Yeah, your Johnson rods are shot, your muffler bearings need to be repacked, and it's time to rotate the air in your tires."

Okay, enough with the car digression. You must find out where you are spending your money, and either reduce spending, or increase income. More about that in the next installment. While you are waiting, however, remember this: an extra dollar earned, because of federal, state, and Social Security taxes, is typically $0.55 to $0.65 more in your pocket. A dollar reduction in spending, however is $1 towards solving your budget problem.

So, now you know what your budget is. You are either spending more than you make, or spending less than you make. If you are spending more than you make--well, you are pretty typical of a lot of people in America. Been there, done that, got the financial scars to show for it. There are three choices: cut spending, increase income, or borrow the difference. (Well, there is the counterfeiting option, but that has its own set of problems--I would strongly discourage it.) Too many Americans take "borrow the difference" as their solution, increasing their credit card debt every month. Some think that they are being clever by opening an equity line of credit to borrow the money at a lower interest rate. Well, it's more clever than paying 18% on your credit card bill, but that's like calling yourself educated, compared to an illiterate. There are circumstances where borrowing against your home equity can make sense--but not to pay for meals out, an oil change for your car, groceries, or your annual vacation to Hawaii.

As I mentioned previously, it is usually better to cut spending, rather than trying to increase income. Increasing your income means that 1/3 to 1/2 of your gain goes to taxes, as part of the government's campaign to make sure that no new rich people happen; reducing spending doesn't enrich the government. There's a place for both actions, however, and we'll cover both of them.

"What's this for?"

"That's the dog's psychiatrist."

"Why does your dog need a psychiatrist?"

"If we leave him in the house, he pees on the carpet. If we leave him outside, he barks and the neighbors get upset."

"You're about to go into bankruptcy. Get rid of the dog!"

Learn to distinguish "need" from "want." Shelter, food, transportation to work and school are needs. Vacation, pets, fancy cars, entertainment equipment, a health club, and yes, dog psychiatrists, are wants.

In some cases, you will discover that you signed up for low easy payments for the next decade to pay for one of your "wants." It may be the case that getting out of that bill isn't going to save you much money at all. Just stop adding to your woes, however, until you get your finances straightened out.

Even in the category of needs, however, look carefully at what you are buying. Most Americans are carrying too much weight. This suggests that while food is a "need," for most Americans, their eating is a mix of "need" and "want." Most prepared foods are expensive compared to buying staples. Yes, pizza tastes better than a peanut butter and jelly sandwich. But you will soon discover that eating when you are hungry (as opposed to satisfying your desire to enjoy a wonderfully tasty meal) will save you a pile of money each month.

Restaurants: ditto. If it's really necessary to eat out, hit the fast food places until your financial woes are resolved--and then go for the smallest and cheapest item that will fill you up. It's amazing how many adults are still eating like they did as teenagers. My son is 15, and like most teenaged boys, he can go through a truly astonishing quantity of food, and still be thin as a rail. I was like that....long, long ago in a galaxy far, far away. At 15, Supersizing the Big Mac Value Meal may be necessary to keep from eating the upholstery in the car; at 25, it's just wasting money, and contributing to long-term weight and health problems. If you doubt this, let me introduce you to the myocardical infarction (technical term for a heart attack) I had at 57, followed by a stroke after they cleaned the plaque out of the clogged artery.

Housing: if you are renting, ask yourself if you would get any benefit from moving to a less expensive place. You should at least look at this possibility, but most of the time, unless you are childless, or are living in an extravagantly expensive place, this really isn't a big win. Look carefully at what you will spend on renting a truck, paying for pizza for your friends to help you move--it may take a long time to save enough on rent to justify it. At least, when I lived in Irvine, I did the math, and concluded a move would take me 13 months to pay for itself--and we ended up being relocated to San Jose by my employer before that point was reached.

There's one other big category of spending reduction, but that's in the segment on interest and credit, so you'll have to wait on this.

"Why, I would be overjoyed to give you a 10% raise! Anything for my loyal employees!"

Okay, back to reality. The best that you can hope for is that your income will rise faster than your expenses. Yes, maybe working a little harder will impress the boss, but that's not one of the more likely strategies to increasing your income. When I was living in Irvine, and confronting financial reality, I was rather stuck. My wife had just had our first baby, and there was no realistic way for her to make enough money to pay a babysitter, and still come out with any net increase in income. (Not that either of us was keen on that anyway.) I went out and found a moonlighting job taking inventories in stores. This was a job that started at 9:00 PM and ended typically about midnight. After working all day long, this was a grueling experience. The pay wasn't much--$7 an hour--but any increase in income without a corresponding increase in spending is a win. Fortunately, another, better moonlighting opportunity came along a few weeks later, doing software development for $20 an hour. I did this for about five months, and the extra money provided the downpayment we needed for our first house.

Make sure that whatever moonlighting job you get doesn't involve driving an extra 200 miles a week to bring in $50 net taxes. That will be a lot of work for little or no net gain. Also make sure that you don't impair your effectiveness at your day job. It is better to work harder and get a better than average raise.

There is a magic secret that enables you get in deep financial trouble very quickly--and get out almost as quickly. This is one of those items that is blindingly obvious--and yet most people don't ever think about, until you tell them.

Let's say that you are a typical American. You spend $4000 a month; you bring home $4000 a month; you have a few hundred in savings, and $10,000 in credit card debt. You never get ahead financially, but at least you aren't sinking. Then, one day, you need to replace the engine on your car--and now, to keep your monthly minimums on your credit cards, you now are spending $4100 a month. As Mr. Micawber would tell you, "result misery." You are now getting further behind every month--and in a few months, even if nothing else goes wrong, you are now spending $4150 or $4200 a month. Soon, you are beginning to watch those ads from bankruptcy lawyers.

Once you have wiped out MasterCard A, it's time to tackle the next one--and here's the magic trick. Take the $400 a month that were spending on paying down MasterCard A--and now apply it to the other credit card with a $5000 balance. You were already putting out $200 a month on that credit card bill, so it will shrink away a lot faster than MasterCard A.

This requires a lot of self-discipline--to stop spending money on things that you don't truly need--and using the money that you have freed up from debt service to pay down other debts as quickly as possible--instead of celebrating. "Whee! I've got $400 a month freed up--I can trade in my Toyota on a Lexus!"

At the time, my sister Susan was getting 9% yield on her money market funds. She was looking for a better return, and I was looking for a lower interest rate. Voila! She loaned me the money at 14.5% APR. She was now getting a better return on her money; my minimum monthly payment dropped. But instead of paying it back to my sister over the same four year repayment term as my credit card, I doubled up the payments, and paid it off in two years. Susan was richer; I was less in debt.

What you need to make this work: a relative, or a close friend, who trusts you enough to loan you money unsecured. You need to offer them an interest rate that is attractive, relative to what they are getting in their incredibly boring and safe money market funds or CDs. However, the gap is still huge. My money market fund is paying me about 1.1% yield right now; my one year CDs are about 2.2%. Interest rates on credit cards are still absurd--12%-18%. Look around--you may find an older relative who has the money to refinance your debt--especially if you can make a strong case to them that this will improve your long-term financial picture, that you are going to aggressively pay down your debts--and that you aren't going to flake on them. (I've lent significant chunks of money to friends and relatives three times; once to pay for an engine repair--almost none of it was paid back; once to my brother-in-law, so he wouldn't lose his mobile home, almost none of it was paid back; once to help some people at church consolidate their debts--most of it was paid back.)

By the way, this strategy really only makes sense for unsecured debt. Car loans are typically financed at rates low enough that this sort of private refinancing isn't going to be a huge win. I think that there may be some liability issues in some states as well on being the lienholder on a car.

It's tempting to use this strategy for putting together the down payment on your first house. The problem is that increasingly, lenders won't allow it--the money has to be a gift, not a loan. My mother was willing to loan us the money for our first house, and did so, but fortunately, by the time we were ready to plunk down the cash, the strategy above had cleaned up our debts to the point where we were able to pay her back, and do the down entirely on our own.

Okay, you have cleaned up your finances enough that all you have is your rent and car payments. What now? Should you cut your credit cards up? No. You just need to be careful what you pay for with your credit cards.

I am at a point now where almost everything that I purchase, other than groceries, I put on my Discover Card. It's convenient (much quicker than writing a check), and I get 2% of my total purchases back from Discover. Should you do this? Hmmm. Maybe not--at least until you are sure that you aren't going to return to the bad practices of the past.

They are a relatively low cost way to amortize larger purchases over a 1-3 month period, especially if writing a check would deplete your savings account. These should be purchases that are necessary, unusual, and that you don't expect to repeat during the time that you are paying for that purchase. Good examples: tires; brake job. Bad examples: groceries; meals out; books. Yes, the interest rate is high, but if you have something that you truly need, use the credit card to finance it over a short period of time. Yes, 18% APR over three months will be about 4.5% that you are paying for that purchase. If you can pay cash or check, all the better. But if paying by cash or check means that you have $28 left in savings, it might be better to pay the interest, and keep your savings account a little healthier to cushion any surprises that come along.

Some people, unfortunately, can't handle a credit card. If you find yourself (or worse, your spouse) charging stuff like groceries, or confusing "want" with "need," it might be best for the credit cards to go into a drawer, and stay there until a legitimate need for them arises. If you really have no self-control, give up the card--but remember that if you have screwed up badly in the past, getting a new credit card might be a lot harder now than it was before.

1. They provide a cushion against unexpected financial disasters.

2. They gather interest (pitiful as interest rates are right now, it's better than 0%).

3. They are a staging area to bigger forms of wealth--like houses.

It used to be a widely spouted rule that you should have six months living expenses in savings. There's certainly some merit to this idea, but this rule seems like it was designed for the era before unemployment insurance, and there was only one person in a family bringing home a paycheck. Today, if you get laid off, unemployment insurance will help a bit. If you are a two paycheck family (as is, unfortunately, now the norm), if one of you loses his or her job, the disaster won't be quite as sudden as it traditionally was for the one paycheck family.

I would encourage, however, the idea that you should strive for having at least a couple of months expenses saved up before you start looking at the next step: buying a home.

But if you are likely to live in the same area for the next several years, and especially if your household income exceeds $60,000 a year, it almost certainly does make sense to buy a house. The reasons are:

1. Equity.

2. Appreciation.

3. Lowered income taxes.

Equity is obvious. If you pay $900 a month in rent, that's all money that is down the tubes. If you pay $1100 a month for a mortgage, most of that is interest, but some of it is payment on the loan principal. You will, after a few years, own some equity in your home.

More importantly than the equity you gain from paying down the loan, however, is that real estate usually appreciates. It doesn't always appreciate--a friend of mine likes to tell of how his family managed to lose money because they bought a house in Malibu, California, and sold it a few years later. People who buy houses during California's periodic panic buying frenzies can find themselves regretting it two or three years later.

In some areas of the country, appreciation is quite slow--or even negative. A figure that is often quoted for the Boise, Idaho area where I live is 1%-3% a year. Where I lived in California, however, it was often a bit higher than that. We bought a house in San Jose in 1985 for $115,950, and sold it in 1987 for $125,000 (3.9% per year). We bought a house in Rohnert Park for $116,000 in 1987, and sold it for $160,000 in 1995 (4.7% per year). We bought a house for $244,000 in 1995, and sold it for $429,000 in 2002 (10.8% per year). None of these are spectacular results for California real estate, but they are all a giant improvement over renting.

Another advantage of buying over renting--you have a pretty good idea what the mortgage is going to be. If you get a fixed mortgage, you know exactly what your payment will be for the next 30 years. Even with most adjustable mortgages, you know the maximum payment for the next several years. This cannot always be said for rent!

I'm not going to try and go into all the nuances of buying houses--there's far more than I can ever tell you, and I won't claim to any great expertise in this area--but I will tell you these items that I have learned over the years:

1. Adjustable mortgages are really, really scary. Why, if interest rates went up 5 points, your house payment could be $1400 a month! However--if interest rates went up that high--and stayed up that high for very long--the whole economy would collapse. Lunatics sometimes get in charge of the asylum in Washington, but they don't hold it indefinitely. In addition, most people refinance their house, or sell, within five years. Calculate what a fixed mortgage will cost you over the next five years--and then what an adjustable will cost your over the next five years, even if interest rates went up so fast that you were paying the maximum possible payment. You'll often find that the fixed mortgage isn't going to be dramatically cheaper. The more realistic scenario--interest rates go up, but not radically--and the adjustable will usually be a bit cheaper. (Be careful, however, about the difference between the "teaser" rate that is in effect for the first six months, and the actual rate you will pay for the following year, three years, or five years.)

2. Don't buy a house primarily for the appreciation. There are too many people who spent too much time watching programs about how to become rich in real estate who ended up in bankruptcy. Buy a house because you need a place to live, and you want to pay yourself part of that monthly payment, not a landlord, and reduce your income taxes.

3. Don't buy the biggest house you can afford. At best, you may find yourself living on beans and peanut butter for the next several years. At worst, you may find yourself out of the house, with a foreclosure black mark on your credit history. You will discover unexpected surprises when you move in. Remember: you are responsible for the repairs--there's no landlord to call up and have fix the clogged toilet, or the leaky faucet. Buy the smallest house that you can afford that meets your needs--even if it is only for a few years. Our first house was 887 square feet, 3 bedroom, 1 bath. It was cramped, but it was brand new, and it was adequate for my wife and our rambunctious toddler.

4. Condos and townhouses may be an adequate substitute for a real house in crowded big cities. They are generally harder to sell than real houses. With condos and townhouses, there are usually homeowners association fees that you have to pay as well--and these can be surprisingly steep. That's just money down the drain.

5. In spite of the hype from people selling timeshare condos, this is not a substitute for a house. Buy the house first. If you want a timeshare condo on the Kona coast (I visited a nice one there when we were vacationing there last year--but we didn't buy), wait until you have bought the house first.

6. If you want a snazzy car--buy the house first. Four or five years after you buy your house, your income will have risen so much faster than your house payment that you will be able to buy the snazzy car without pain. Trust me on this. I spent too much money on new cars when I started working at 18, and not enough saving for the house.

The 2017 tax law changes increased the standard deduction for a married couple to $24,000. Unless you have a huge mortgage or are making charitable contributions in the $20,000 a year range, the standard deduction is a better deal than itemized deductions so you might as well pay off the mortgage. My wife and I did so in January of 2019. The credit union mortgage officer admitted this was unusual, except we were the third that day. I guess the word got out.

The 2017 tax law changes also limits how much property tax you may deduct as well. You may no longer deduct more than $10,000 in state, local, and property taxes. If you live in one of the coastal states, and have a high income and expensive house, this means that you get less benefit from the property tax deduction than before. It also allows you to deduct interest on only the first $750,000 of a mortgage. This is why the Democrats so strongly opposed Trump's tax law change--their donors were hurt.

When I first started mulling this series over, I didn't even think about this topic: financial struggles with your spouse. I received enough emails suggesting that I deal with it--because they were dealing with it.

I'm going to keep this short and simple, because this is only partly a financial planning problem; it is mostly a problem of your relationship with your spouse. Almost any advice I can give about how to handle financial disputes with your spouse is going to be wrong for some of you.

There are a lot of causes of this tendency. In the case of this particular guy, the problem was probably two factors combined: he came out of a physically abusive home with an alcoholic father; he had been sexually abused by a Scoutmaster as a child. Children growing up in alcoholic homes often have trouble with the notion of causality--that action A results in result B--and that this is likely to be a repeatable phenomenon. Why? Because in homes where alcohol is a major influence on people's behavior, there is no causality. The mother or father who is sweet and concerned one evening may be a violent, raging monster the next. You can't predict the future because the past makes no sense. You've got an extra $200 this month? Quick, spend it! It may disappear over night! The sexual abuse had also left some very serious scars on this guy. In some respects, he had never grown up. Again, this is no surprise. I know several dozen child sexual abuse survivors (remember, I'm from California), and all of them, to one degree or another, are still exhibiting signs of that damage. Difficulties with emotional maturity seem to be common.

Of course, not every spendthrift has deep and dark secrets driving them. Some people just don't like to exercise the self-discipline that says, "I don't really need this." Others become convinced that they are never going to have anything anyway, so why bother to save? (I speak from experience on both counts.) Persuading a spendthrift spouse to rein in their unnecessary spending is a very, very hard thing to do. If there are some deep dark secrets driving this behavior, professional counselling may be in order--but I wouldn't make that assumption, especially in a society that encourages spending and materialism as a way to achieve happiness. It almost never does provide happiness; at most, your latest purchase is a short-term distraction--and then you feel the need to spend again. A friend of mine calls it "retail therapy."

In the especially brutal form, this is done surreptiously. If you have good credit, this can escalate to a point where a financial crisis makes bankruptcy look like a good idea. Most of the time, it's a bit more restrained than that, and just leads to increasing resentment. Sometimes, neither party sees their complicity in this. "Everything I buy is reasonable and necessary; she's the spendthrift!"

Sometimes, this spending frenzy is the result of an agreement: "I want new furniture for the living room; you can go buy that milling machine you want." This is an improvement over the retaliatory purchasing approach, but something you need to think about when you get to a point of negotiating extravagant purchases with your spouse: would I rather have new living room furniture this year, or would I rather be wealthy in five or ten years? The choice is yours.

The only longitudinal studies that I have seen about the effects of divorce on the kids suggest that you are going to be putting out money to help them through their feeling of abandonment and responsibility for the divorce. I've also personally seen a lot of these damaged kids. Divorce: it's a luxury that you can really only afford when you get really, really rich.

I've watched (from a painfully close distance) dozens of marriages break up. I've only seen a couple where the divorce was really necessary (spousal or child abuse; repeated infidelity). Quite a number of these divorces can be laid at the feet of a materialism that says, "We gotta have all those toys that everyone else has!" The result: husband and wife both working their tails off, coming home exhausted, then Mom cooks dinner, helps the kids with their homework, and does the laundry. By the time Dad and Mom crawl into bed, he's ready; she's just ready to go to sleep. Eventually, Dad meets a woman who isn't too tired for sex, or Mom meets some guy who listens to her complaints sympathetically. Shortly thereafter, Mom tells Dad to move out.

Here's the hardest question I am going to ask in this entire series: how important are those toys you want to buy? Is it worth you and your spouse being so exhausted that you have to make a weekend getaway to make love? You are both working too hard. As our kids were growing up, my wife stayed home and raised our kids. She was there doing the housework, dealing with plumbers, taking the kids to doctors and dentists, sitting on hold with insurance companies. I was able to devote my full energies to my job. Are you surprised that our marriage held together, and most others did not?

A lot of people misunderstand how much extra they are gaining from having both parents working full-time. If Mom is working full-time, grossing $3,000 extra per month, on top of Dad's $3,500 a month, how much extra do they actually get to keep? Perhaps $3,000 extra a month. Out of this, you have the commuting costs, day care costs (if the kids are still small), extra money on clothes (if Mom has to get dressed up for her work), the cost of lunches out--and then, because both of you are exhausted at the end of the day, a lot more dinners out, or pizzas delivered. Yes, there is actually a net gain from Mom working--but once you figure in those other costs, you may be astonished at how little it turns out to be.

Your personal equation is going to be dependent on what you do for a living. If your paycheck is $5,000 per month, even after paying those bills, the job will contribute significantly to your wealth--but there are a lot of Moms out there whose gross income is more like $1,500 a month, probably netting, after taxes, commuting, and day care expenses, closer to $600 a month. You should consider whether you can cut expenses instead. Can you operate with one car instead of two, if one of you isn't working? For a number of years, my wife and I had one car. I walked or took the bus to work most days; sometimes she would drop me at work and pick me up. (Obviously, this only works if your job is close to home.)

Now, it's true that a stay-at-home Mom (or Dad--your choice) isn't a guarantee of a successful marriage, and there is certainly a price to pay in reduced income. But from what I have seen, the model of two full-time working parents while the kids are small leads to divorce far more often.

I am reluctant to get too specific about the sequence to follow on this, because everyone has slightly different situations. If you are single, or you and your spouse aren't planning to have kids anytime soon, buying a house may not make sense immediately. If you have a low income--and are therefore in a low marginal tax bracket--it may not make sense to buy a house either. What I intend to do is show you the sequence that my wife and I followed, as modified by what I have since learned.

Of course, you don't just put in $100 once; you put $100 in every month. If you start early enough at this, it turns into a huge pile of money. Start at age 22. Put $100 a month into your 401(k). If your 401(k) averages 8% return (which is not a terribly high return, when you consider the last 60 years), it will have $299,470 and some change when you retire at age 60. I cannot emphasize too strongly how important it is to get started early. This is one of the few cases where time is on your side. Instead of starting at 22, what happens if you start contributing at age 32? When you retire at age 60, instead of $299,470, you have $126,621--or less than half the amount.

But in what sort of mutual funds should you invest your 401(k) money? The traditional model says that a young person should invest in the most aggressive stock growth mutual funds (which exchange high risk for high yield). As you reach your 40s, you start to move the money into more conservative stock funds. As you approach retirement, say, in your 50s, you move most of the money into bond funds (which have disappointing returns, and lower risk), and then, when you are ready to retire, any additional money going into your 401(k) should be in money market funds (almost no return, but no real risk).

There's a lot to be said for this model--and I kick myself that when I first start contributing to a 401(k) in the mid-1980s, I put everything into bond funds. I was so scared that the money might evaporate away. Even into the early 1990s, I was still far too heavily weighted towards bond funds and conservative stock funds. If I had followed the traditional advice on this, I would have benefited from the most amazing stock market boom in history--the 1990s bubble--and I would probably have another $200K-$400K in my 401(k) account than I have now.

However: there is something to be said for being cautious, especially when you are living in "interesting times." (There is supposedly an old Chinese curse, "May you live in interesting times.") A lot of people saw their 401(k) funds drop quite impressively in value since May of 2000, as the stock market bubble deflated with all the charm and grace of a tire running over a nailstrip. I think it is likely that over the next two to three years, all of this will be a painful memory (for most Americans). Those who cashed out their 401(k), or who had to retire, or moved 401(k) money from stock funds to bond funds--they are never going to forget this experience--and not in a positive way. DO NOT PANIC IN A BEAR MARKET! This not only wipes out the advantages of the bull market that you just enjoyed, but you, along with millions of other nervous nellies, cause the market to sink even faster, because you are trying to sell when others are doing likewise. The time to buy is when others are losing their heads in panic; the time to sell is when others insist that the market can only go up. (Thanks, Abby Cohen, the stock analyst who was talking about Dow 20,000 just before the 2000 crash, and persuaded me to stay in the stock market. Yes, that "thanks" is sarcasm.)

I was about 15 years away (I have since retired) from the magic age where I expected to start using some of that 401(k) money, so I had been allocating my new contributions to medium-term bond funds--funds that invest in corporate and governmental bonds that will come due roughly when I will start to draw down on that money--and very conservative stock growth funds (the kind that emphasize stocks that pay a regular dividend). I generally leave money that is already in existing funds in place, hoping that the managers of those funds are smart enough to make sensible decisions with the money.

I still think that people in their 20s should be investing primarily in stock growth funds--but I would emphasize growth funds that buy stocks in blue chip companies--the kind that pay dividends; not the funds that invest in companies that have never made any money, but that everyone knows are going to be worth a lot one of these days. Yeah, those days of high tech companies losing piles of money while their stock rises 800% a year will come again--but it seems like a pretty risky thing to put much money into. This isn't play money; you are going to need this to pay for your health insurance in 30 years.

I emphasized "hoping that the managers of those funds know what they are doing" a couple of paragraphs ago. This is one of the reasons why I think it is best to have the money in your 401(k) plan distributed among several different plans. I don't think it is likely that any of these mutual funds is going to make the headlines when the fund manager cashes out everyone's money and moves to Brazil. Mutual funds tend to have lots of checks and balances to prevent that sort of thing. But it is not unknown for mutual fund managers to make very, very poor decisions--and it would be nice if only 10% of your 401(k) money ended up disappointing you, instead of 100% of it.

You may not have access to a 401(k) fund at your employer. There are Individual Retirement Accounts available to you. I don't know enough about them to tell you much, however. (Well I could, but I might well mislead you, and I would rather not do that.)

Some people get especially screwed on this because they take the money out when their job evaporates, live on it for a few months, and forget about the tax problem. Come the following April, they are scurrying around looking for $10,000 to pay to IRS and their state income tax agency.

Another really amazing behavior that I will mention, because

I've heard

of people doing this: a guy leaves a job he has held for 15 years to go

to work for a startup. He takes a huge wad of money out of his 401(k)

plan

because he is convinced the startup is going to make him rich. He buys

himself a very fancy car (so he doesn't have to wait for the startup to

be successful). The startup makes him a very disappointing amount of

money

(if it doesn't just go down the tubes, like my last startup did).

Whoops!

There went $65,000 on a fancy car--and it's not going to be available

for

his retirement in another 20 years. Dumb, dumb, dumb.

Bonds, stocks, mutual funds, money market accounts--what are all those things? Today we will start to cover bonds.

Until you have $20K-$40K sitting around with nothing to do, I would not encourage you to buy bonds of any sort. But: you need to understand bonds in order to understand bond mutual funds. We'll get to mutual funds in a later segment; you need to understand bonds and stocks first, because most mutual funds are built on top of bonds and stocks. Bonds are enough of a struggle to get through that I'll take two segments to get through them, followed by stocks, then by mutual funds.

A bond is a loan to a government or corporation for a certain period of time at a certain interest rate. As an example, I had some 30 year Treasury bonds that are due November 15, 2016. When the U.S. government first sold these bonds in 1986, they sold for $1000 each. (That's also known as the par value or face value.) The U.S. government promises (cross their heart and hope to die) to pay 7.5% (or the coupon rate) of the par value as a dividend every year. This dividend is actually paid in two halves--one half on the anniversary date, November 15, and the other half on May 15 (six months later). When the bonds are due, on November 15, 2016, they will make the final dividend payment, and the par value of the bond.

Now, this isn't like a marriage; you can sell a bond before maturity. (Okay, maybe it is like a marriage.) At any given time, there are people trying to sell bonds, because they want the capital out of them; there are other people who are buying bonds. As it happens, I was one of those people that was looking to buy bonds back in 1997. My first, very nervous foray into long-term investing, was to buy those Treasury bonds from someone who had bought them when they were first issued.

If bonds were a straightforward loan, this would be simple to understand. But there's a little complexity here. It turns out that interest rates rise and fall--but the dividend that the government promised when they issued that bond doesn't change. If you think about this for a minute or two, you'll realize that a bond that pays 7.5% interest--and has the full faith and credit of the United States government behind it--is really, really good today. If you tried to buy new government bonds today, you would be lucky to get 2% interest. So, these older bonds, that pay much higher interest rates, are in high demand. What happens to the price of a bond that everyone would like to buy? The price of the bond goes up. You must pay above par in order to buy that bond. The dividend each year will still be 7.5% of the par value of the bond--but you now have to pay $1300 to buy that $1000 bond. You'll get $75 a year in interest for the next 13 years, but in 2016, when that bond is redeemed, you will have lost $300. This goes the other way, too. If interest rates rise, a bond issued today that pays 4.5% dividend is going to be unattractive to bond buyers. Its price will fall.

This leads us to the concept of "yield to maturity" (YTM). If you buy that $1000 par value bond for $1300, but it pays 7.5% of the par value each year, how much will you make on this bond, including both dividend payments, and the change in value of the bond from now to when it is redeemed? This is the annualized YTM--the yield divided by the numbers of years left. (Watch carefully--you will sometimes see YTM listed for a bond that has less than a year left. This may not be the annualized yield to maturity.)

So, if you want to make money on bonds, you buy when interest rates are high, and sell when interest rates are low, right? Well, you can do that. If you hold a bond for more than one year, the difference between the purchase and sale price is taxed as a long-term capital gain. Long-term capital gains are subject to a maximum 15% federal income tax rate--for most well-paid people (the only sort who are going to be buying and selling bonds), this is a big improvement over the 28% or 31% federal income tax rate. (The states, however, don't necessarily follow the federal rules on this. Idaho, for example, taxes capital gains as ordinary income.) If you have a really good crystal ball, the strategy could be: buy bonds when interest rates are high, and earn high dividends; sell the bonds when the economy is in recession and interest rates are low; put that money into savings; wait for interest rates to go up again, and take the money you earned from the dividends and the capital gain on the bonds, and buy more bonds.

The problem, of course, is that good crystal balls are in short supply. Had I realized that interest rates were going to be this low, instead of buying 50 of those Treasury bonds, I would have bought 200 of them. I had the cash available at the time, but I didn't have the guts to do it. Later, I looked at those 50 Treasury bonds, and I was tempted to sell them while interest rates remained low. I paid about $47K for them; I could have sold them for about $65K. Of course, that would mean paying about $4900 in capital gains taxes to the federal and Idaho governments, and giving up that lovely $3750 a year in dividend income.... When I ran the spreadsheet, it told me that I would have to reinvest the money in a 6.6% YTM bond next year to break even with this strategy--and I did not expect to see Treasury bonds with yields that good over the next few years.

Generally, the reason to buy bonds is for the dividends. There are people that make a living buying and selling bonds. My own calculations suggest that unless you are doing this on a pretty large scale (millions of dollars in bonds), and have somewhere interesting to park the cash when interest rates are low, you are better off buying bonds and holding them to maturity. There are a couple of interesting exceptions, however, which I will now discuss.

Some years ago, having watched the stock market sit in the doldrums, I decided to sell off some of my worst performing mutual funds, and move some of my spare cash, into bonds. But interest rates were low. Buying bonds with long maturities would have meant low interest rates, and the danger of the prices falling when interest rates start to rise again (as I expect that they will in 2004 or 2005). On the other hand, letting this money sit in a money market fund at 1.1% interest just wasn't attractive. So I bought bonds with relatively short maturities; some AT&T bonds due in 2007; some Capital One Bank bonds due in 2005; some Ford Motor Company bonds due in 2007; some Verizon bonds due in 2005. These were all short enough maturities that if rising interest rates sneaked up on me, I could sell them and buy long-term bonds without much danger that my short-term bonds would fall dramatically in price from what I paid for them last year. If worst comes to worst, I can just sit on these bonds until they come due. The Ford bonds and the AT&T bonds, for example, have an annualized yield to maturity exceeding 7%. I can live with that!

Down from this are U.S. Government agencies, such as the Government National Mortgage Association, Federal National Mortgage Association, Student Loan Marketing Association, and a bunch of others that I can't even begin to keep track of. These are commonly referred to by "cute" abbreviations: Ginniemae, Fanniemae, Salliemae. (Hurricanes used to all be female; now that seems to be reserved for government credit agencies.) These don't have "full faith and credit" behind them, but I get the impression that very, very few bond professionals believe that the U. S. Government would let any of these agencies go down the tubes. Just to make this confusing: the minimum denomination on these bonds is $10,000.

There are also what are commonly called municipal bonds. These are, as the name implies, usually issued by cities, but also counties, states, school districts, and all the uncountable government agencies that you don’t even realize exist until you start reading through these lists of bonds. Most of these “municipal” bonds are backed by some government agency. Some are incredibly tiny operations that startle you to discover even exist; others are used by states like California and New York to finance airports and other major projects.

Municipal bonds aren’t like U.S. government bonds in a couple of very interesting ways:

1. They can default—meaning that you don’t get your money out. We’ll discuss defaults, insurance, and ratings below.

2. The income from these bonds is (usually) exempt from federal income taxation, and from state income taxation for that state. This means that if you live in California, and you buy San Francisco Airport bonds, the interest is exempt from federal and California state income taxes. If you buy Oregon bonds, and you live in California, you are only exempt from federal income taxes on the interest. That’s still a pretty good deal—but as a consequence, the interest rates are much lower than a U.S. government bond, or a corporate bond. If you are making $100,000 a year, the lower interest rate is probably a reasonable trade-off for the tax exemption; if you are making $40,000 a year, you are better off buying U.S. government or corporate bonds, and paying the income taxes.

Let’s talk about that matter of bond defaults. Corporations and government agencies issue gobs of bonds. If corporations and local governments, like the U.S. government, never went bankrupt…well, there would be a lot of winged pigs overhead as well. When a corporation or local government goes under, bondholders get paid (usually) before stockholders, but after IRS, and employees asking for their back wages.

Fortunately, it’s not a crap shoot—well, not entirely. It turns out that there are two private firms that examine the creditworthiness of both local governments and corporations: Standard & Poor’s, and Moody’s. They have different ways of rating bonds, and of course, incompatible ways to describing those credit ratings. I don't know enough to give you a clear picture of why you should trust one over the other, but essentially, consider these pretty good ways to know whether your bonds are likely to be repaid, and remember that neither firm employs mind readers.

As a general rule: highly rated (S&P A and above) corporations do not default, and even those corporations that start out A don't work their way down to the lower ratings very quickly. It can take years for an S&P A-rated corporation to sink to the point where you have to worry about it.

Another rule: S&P Baa rating is considered the bottom of "investment grade" bonds. Everything below that rating is considered a "junk bond." That means that you are earning a lot higher interest rate in exchange for a lot more risk. Junk bonds have some of the same risk potential of playing the stock market, but seldom the opportunity to get rich.

So, what happens when you buy bonds? Keep your eyes wide open. If you buy corporate bonds that have a long maturity, there is the real possibility that the corporation could get to the point, five years hence, where you might find your bonds are keeping you up at a night, whispering, "Default risk." The smartest thing to do, however, is to buy a diversified portfolio of bonds: not all in the same industry, and certainly not all in the same corporation. This means that if one of your bonds is defaulted, you aren't completely wiped out.

I haven't done the best possible diversification. (Learn from my mistakes.) When I first started buying corporate bonds last year, I was so taken by the yield (exceeding 7% annualized yield to maturity) on some Ford bonds due in 2007, that I bought $150K worth of them. Subsequent purchases of corporate bonds have been in smaller chunks--$30K or $50K per bond. But because I have so much tied up in an automobile industry bond, I am reluctant to buy any GM bonds (which are usually somewhat lower yields). Ford and GM aren't likely to both go belly up, but let's say that someone perfects the teleportation disks in Larry Niven's novels....

Another problem is that some municipal bonds are actually

financing

private ventures that some government agency has talked themselves into

believing are good for the public. These private venture municipal

bonds

have some quirks concerning the tax-free nature of the interest that I

am not sufficiently knowledgeable about to discuss--but I know that

they

can surprise you at tax time, especially if the dreaded phrase

"Alternative

Minimum Tax" is part of your tax return. (Been there, almost done that,

avoided it by careful exercising of stock options partly in one year,

and

partly in the next.)

Stock is partial ownership of a corporation. If you buy stock in a company, you are either buying it directly from the company, or from someone who bought it from the company, or someone who bought it from someone who bought it from the company. Regardless of how many steps you are removed from the initial sale of the stock by the company, the net effect is the same: buying stock provides capital that allows the company to build factories, purchase materials to turn into a product, hire engineers to design a product, or one of the thousands of other necessary and sometimes unnecessary things on which companies spend money.

What do you get when you buy stock? There are only three rational reasons to buy stocks: dividends, capital appreciation, or control. You may find that the stock you purchased only gives you one of these three items. (If it doesn't give you any of the three, you probably shouldn't be buying it.)

1. not profitable;

2. had never made a profit;

3. didn't see a profit coming anytime soon;

4. so everyone and his brother bought the stocks, and drove them to truly insane levels.

What's going on with that? If you think a company that sells for $20 per share will be selling for $40 per share in six months, why do you care that they aren't making any money? After all, you'll double your money in six months! Okay, but why will the company's stock double in value in six months? Because everyone is buying it with that expectation. And what happens if, one beautiful morning, enough people get nervous that this can't go on forever, and start selling? Hmmm. No dividends because no profits. The stock stops rising in value. I guess I better sell. So why will anyone buy the stock that you are trying to sell? I guess they won't, will they? And you know why the great bubble of high-tech collapsed in April of 2000.

You buy a stock like GM for the combination of dividends and capital appreciation. The two, of course, are related. If GM's profits go up next year, and they raise the dividend, it makes the stock more attractive. This encourages people to buy GM stock, and drives up the price. If GM's profits fall, and they lower the dividend, some stockholders will say, "Why am I holding a stock with a poor dividend--and a falling stock price?"

Preferred shares have one other great advantage over common stock (something I have learned since I first wrote this): they often have a very high yield, and relatively stable stock price. The stable stock price is because the high yield doesn't change much, so they have many of the advantages of a corporate bond. Preferred stocks are callable like bonds at a specified price and earliest call date.

If you buy a preferred stock above the call price, you might lose money. Just make sure the earliest call date allows enough dividends to cover the potential drop between purchase price and call price. I generally buy preferred stocks if they are below call price, with the hope that if called, I will get the dividends in the meantime and a profit on the stock price. As an example, I recently bought GENERAL ELEC CAP CORP NT 53 GEH:NYSE, a preferred stock with a 4.88% annualized yield. Not a spectacular yield but I was trading trading yield for long-term security; I can't picture General Electric going under. I bought at $24.96 on 11/25/2016, below its call price of $25 per share. The next possible call is 01/29/18, so I can be sure of getting some okay dividends over the next year plus two months. As a high-yield example, I also bought BCS/PRD:NYSEADR, preferred stock of Barclays Bank below the $25 call price. It has been paying over 8% annually ever since.

Stock brokers make their money on the transaction charge involved in buying and selling stocks. If you buy a stock at $20 a share, and resell it at $21 a share, there are two possibilities:

1. You are selling such a huge number of shares that the broker's commission is noise.

2. You are selling such a small number of shares that the broker's commission is as big as your net profit.

Either way, this is a sobering reminder that if you plan to make money "day-trading" (as the rapid in and out of stock trading is called) you need at least one of the following:

1. A discount broker with very low commissions.

2. Enormously good skill in identifying stocks that are undervalued.

3. The ability to forsee the future.

4. Enormous guts.

My very first stock trading exercise was when I was 16 years old. I had become enamored of Interdata Corporation for the reason that only a teenaged computer nerd would: I loved the instruction set of their minicomputers. So I bought 15 shares at $9 a share. (In my family, this pegged me as an aspiring Alex Keaton--for those of you who remember the series Family Ties.) A few months later, Perkin-Elmer Corporation bought Interdata. During the run-up in Interdata's stock price, I sold those 15 shares for $18.75 per share. The broker's commissions were more than my net profit. I made about $60 profit from my incredible foresight (actually, just dumb luck).

In 1993, I was a pretty active day-trader. I spent a lot of time plotting the price and volume of DSC stock, day to day. DSC had acquired my employer, Optilink Corporation, and my Optilink stock options had become DSC stock options, so this was more than an academic exercise. In addition to my stock options, I was also buying and selling pretty gutsily (or stupidly) large blocks of stock: 500 and 1000 share trades, when the stock was in the range $40-$65 a share.

Because there were large traders that had computers placing buy and sell trades based on arcane theories of price movement, DSC stock was often engaged in something that looked like a drunken sine wave, with a period of 1.5 to 2.5 days. I was trying to buy at the bottoms, and sell at the tops, and on average, it worked pretty well. I was making $1000-$1200 per trade (when it worked) and losing $500-800 per trade (when I guessed wrong). It was, however, very rough on my stomach--these were huge amounts of money for me back then, and even today, this level of day-trading for someone at my wealth level back then was, in retrospect, insane.

To top it all off, because all of these capital gains were short-term (measured in hours and days), 40% of the profit was going to taxes. Why bother?

Well, along with the stomach-wrenching moments watching the stock rise and fall (distracting not only myself, but lots of other engineers from what we were supposed to be doing during the day), there was an adrenalin rush to it. If you have read Tom Wolfe's The Bonfire of the Vanities (a splendid novel about New York City), you may recall the expression that the bond trader describes himself with: "He-Man Master of the Universe." (I've since read that this is actually a very cleaned up version of what real Wall Street sorts call themselves--but I'm too polite to use the expression that they use.) I was at least a "He-Man Master of My Neighborhood." It was a heady feeling, and if I was not such a risk-averse person, might have been led into the sort of nonsense that sinks day-traders with more guts than sense.

If you buy stocks directly, rather than buying a mutual fund that buys stocks, remember:

1. Any individual stock involves significant risk. (although preferred stocks involve much less) Even if the average of the stock market rises, the individual stocks that you buy could plummet very unexpectedly because of dishonesty in accounting that has just been discovered. The company may make mistakes (the infamous exploding Pinto gas tanks problem of Ford). They could get stuck with the bill for something that they didn't do, but the courts found them a convenient deep pocket. Sometimes, stocks fall for no apparent reason, other than a lot of investors simultaneously decide something else is sexier.

2. If you are buying stocks based on rumors about a new product, the chances are excellent that what you are hearing are the result of a "pump and dump" specialist--someone who buys a stock, circulates rumors about how well the company is doing, or is about to do, waits for you and the other suckers to drive up the price--then they dump the stock at the higher price. Once you (and the rest of the market) find out that the rumors were false, the stock has fallen back down again. I get at least four to five rumor emails a week that are obviously "pump and dump" conmen, trying to provoke a buying panic in some low-priced stock.

3. You can get around the problem of large stock commissions by buying really large blocks of stock--but usually, this means that you need to buy a low-priced stock. A stock that sells for $3 a stock means that you can a thousand shares very cheaply. If the stock goes up a dollar in value, you can sell it, and even after paying the brokerage commission, you can make more than $900. The problem is that a lot of low-priced stocks are low-priced for a reason.

Our next segment will discuss why it is generally a better idea to buy stocks through mutual funds--and explain what mutual funds are.

Every so often, it is good to examine your portfolio. In my case, there are a number of stocks that I purchased for their high dividend yield. Some have risen a bit in value; others, such as SPH and FTR, have dropped a good bit. So does it make sense to take my losses and reinvest that money in a mutual fund?

Curiously, what made those high-dividend stocks so attractive is often even more the case at the lower stock price. At SPH's current $24.02 price, the annualized dividend yield remains 14.64%. FTR now at $14.31 still has a 16.72% yield. One tragedy of my portfolio, AT, has dropped dramatically because they stopped paying dividends some time back, amid allegations of intentional misrepresentation of their earnings. The question is whether to shoot this dog and reinvest that money, or hope for the stock price to rise.

Dog shooting is often done at the end of the year, because capital losses offset capital gains (up to a $3000 capital loss for the year; beyond that point, the loss carries over to subsequent year capital gain calculations).

But even if you don't have the courage (or is it insanity?) to invest in the stock market--you may be better off borrowing for a car, and keeping the money in savings. I recently (late December of 2008) bought a 2005 Jaguar X-type--and got a spectacular price on it (less than $16,000, plus title and sales tax). I could have paid cash--but in November of 2008, I had put money into some five year Certificates of Deposit with a 4.30% annual yield. I ended up with an interest rate of 5.24% on a five year used car loan. So even though the interest rate on the car loan is higher than the interest rate on the CD--I came out ahead taking a loan.

The interest on the CD is taxable, of course, but assuming a 33% marginal federal and state income rate, over five years I will still earn a net $2943.55 in interest income. The total interest paid over 60 months on the car loan is $2458.23. (Remember that the interest you pay on a car loan is on the declining principal balance--while the interest earned on the CD is on the accruing balance of principal and interest.)

Okay, that's a net gain. If I had paid cash for the Jaguar, by taking money out of the CD, I would have paid no interest on the car loan--and I would have put $335.97 per month into savings, and gathered interest on that rising balance. What interest would the $335.97 per month payment accrue over those 60 months?

Remember that the 4.30% APY CD was because I locked that interest in during November--and I would not get that interest rate today--and the way things are going, not likely again for another year or more. Also, that rate required me to lock it in for five years. While some of the early car payments could be locked in for five years, and get a roughly similar situation, the vast majority of those payments would be in the second, third, fourth, and fifth years. Unless I was locking up that money for five years (which is not a comparable situation), I would never get 4.30% APY--not even close. Furthermore, my credit union has a minimum $500 balance to get CD rates that high, so at least every other month I would just have the money sitting in a demand deposit account, at a much lower rate.

If I managed to earn 3% a year on the money that would otherwise be going to car payments (which seems extremely unlikely, with current interest rates), I would only have a net interest income of $1029.11 over five years--and I would be forgoing the $2943.55 net interest income that the $17,700 would have earned in the CD.

So, if I keep the money in a CD, and make payments: $2943.55 CD income - $2458.23 car loan interest = $485.32 net income. If I had paid cash, and broken a couple of CDs: $1029.11 net interest income (and that is making the optimistic assumption of 3% yield) - $2943.55 lost CD income, for a net loss of $1914.44. Even with a completely unrealistic 6% yield as I put those "car payments" into savings, this still comes to a net loss of $815.99 over five years.

So, what about the supposed rule that you should never make payments, if you can afford to pay cash? If there is a big difference in interest rates between CDs and loans, this might be true. Under some economic conditions, this might be true. If you don't have a spectacular credit score (my FICO number is 819), you may get stuck with such a high interest rate that you would be better off paying cash. But my guess is that many people that can afford to pay cash for a car probably also have a pretty decent credit score. (Okay, drug dealers might be the exception.)

More recently, I bought a Jaguar XF and because I was able to get a 2.3% interest rate on the car loan ( by then my FICO score was 850); I took it. Interest rates on CDs were dismal when I bought it but when I later considered liquidating the CDs and paying off the loan, I discovered it made more sense to break the CDs one at a time, put the money in savings, and arrange automatic transfer of the car payments from savings. Paying off the loan was about $2000 more expensive than breaking CDs as needed and making payments.

I am adding the spreadsheet for modeling the X-type loan here. This should apply to any loan where the interest is not tax deductible. Houses and student loans require different treatment--I may work on that as I feel more energetic.

Pretty regularly, I get breathless emails about buying gold or silver, because either intentionally or because of gross incompetence, the banksters are going to destroy the world economy, and we are going to be reduced to eating rats to survive. The ads you see on cable TV (at least on Fox News) are a bit more subtle, but still preaching the same message: buy gold or silver now to make big profits and protect your wealth.

This is a a scam. Let me explain. Gold and silver are not investments; there is no return on your gold or silver except for increases in prices, and neither metal reproduces (unless you have the rare organic gold). At best, gold and silver are inflation hedges. If there is a 10% inflation of the money supply, your gold or silver will likely appreciate in value 10% relative to the dollar. But you are not going to get more than inflation related gain. If demand for either metal increases (say, from $1200 to $1500 per ounce for gold), you may get a net gain of 15% (25% appreciation minus 10% inflation), but such a growth is only likely if lots of people suddenly start buying gold in such quantities that it increases the inflation-adjusted price. In practice, war is one of the only certain causes of gold price increases.

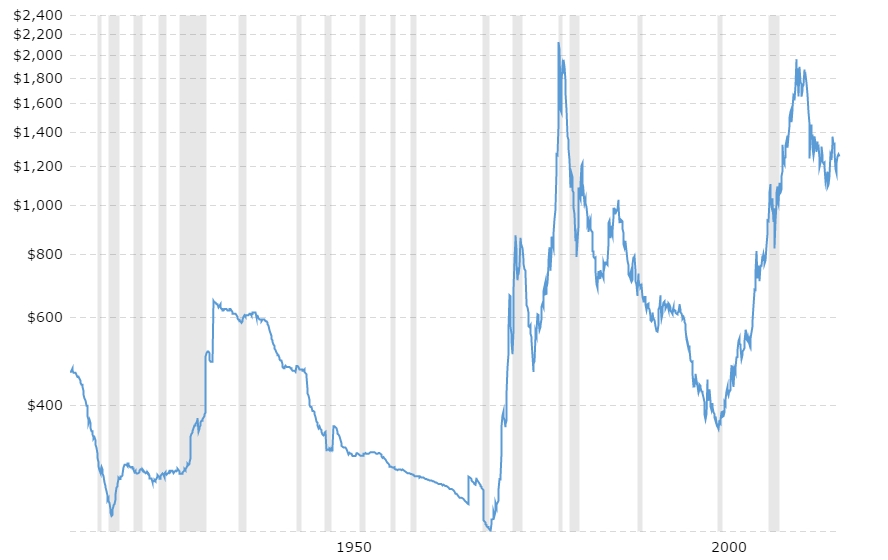

Gold prices over time:

There are two big peaks on this chart: one when I bought wedding rings in 1980; the other in mid-2011. If you bought $2100 of gold in 1980, in 2001, it would be worth $373, and that is inflation-adjusted. Similarly, $1697 of gold bought in August, 2011 would be worth $1216 today (again inflation-adjusted). Yes, buying at the lows and selling at the highs would be very profitable, but similar investments in stock mutual funds would have given similar results with less risk.

Silver:

In December, 1979, the Hunt brothers tried to corner the world silver market, driving up prices to $102/ounce and losing $750,000,000 in the process as the price plummeted, eventually losing all the billions their father (an oilman who brought his lunch to work and drove a beat-up pickup) had left them. By 2001, it was back to $5.76/ounce, a historically typical price. There was a similar run-up and collapse with gold in 2011. A personal story: my sister and brother-in-law had a small quantity of silver coins inherited from our Depression-era mother. They were trying to sell it some months ago when silver was briefly $20/ounce. Now it is $16.84/ounce. Some precious metal nuts said to keep it because it had to go up. Glad they sold it at $20/ounce.

For people with nothing, buying precious metals as a economic collapse idea might make sense, but even then ammunition and guns makes more sense: these have practical value in a Mad Max world. While gold and silver have very real industrial uses, they are pretty well useless to most people except as a currency. Ammo and guns are immediately useful to everyone in a post-apocalyptic world.

Buy cheap guns, by the way. Many years ago, I talked with a guy who came to America from post-war Germany. In the postwar chaos, he said his wife's jewelry was more useful than gold bars. (I was too polite to ask how he obtained gold bars.) "Have you ever tried to get a haircut with a $50 bill?" Today, substitute $100 or $500 bill.

What is driving this gold and silver madness? Yes, these are both very pretty metals when polished. (With silver, plan to polish it regularly.) Some of this are people with limited understanding of economics and finance. Some of this is the gold and silver firms, cashing in on fearful people. If you are dirt poor, gold and silver are highly risky inflation hedges. If you are obscenely rich, they are bad investments compared to your multimillion dollar survival condo and 100,000 rounds of 9mm. If you are middle class, keep putting money in your 401k and maybe buy an extra 1000 round case of 9mm occasionally.

The sky is unlikely to fall. Do not reach 65 relying on a piddling Social Security check. You want half a million minimum in your 401k when you retire. My wife reminded me of the Twilight Zone episode where the criminals steal an armored car of gold and spend a 100 years in suspended animation waiting for the heat to die down. When they wake they have to get out of Death Valley on foot. The last survivor tries to get help by offering a gold bar to some passers-by. The wife says, "Wasn't gold worth something once?"

The larger issue here is fear. A lot of people spend their lives in often irrational fear.

I am now retired. The heart attack and stroke at 56 disabled me from my occupation of software engineer. (That part of my brain did not survive very well.) Not quite the disaster it sounds; I was planning to retire at 59 1/2 when I could start drawing from my 401(k). Disabled means that I get a Social Security disability check, very near the highest level that they pay. The $200,000 I put into Social Security (and the matching taxes my employers put in) over 30+ years could have been better invested by myself, but at least I get something back for it. I am withdrawing 5% a year from my 401(k), and when the time comes that I need it I will do the same from my Schwab account. Because both accounts will almost certainly grow 8%-12% a year (still invested in stock mutual funds in the 401(k) and high-dividend stocks in the Schwab account), I can later increase the amount I withdraw if I need it, and likely leave a million plus to my wife and thereafter to our kids.

Since I wrote this, my IRA has grown 37% (even while taking out 8% per year). I have since started taking out 6% per year of my now larger IRA. I expect to continue increasing the amount (8% of the new higher balance) every year or so, improving my standard of living. I still hope to leave a million or more to my kids.

How is my retirement? I bought a new 2014 Jaguar XF I get to do what I love (historical and legal work for NRA and writing books and running my small manufacturing business for telescope accessories. I have since sold this business to an American living in Poland. (You can make up to $1373 per month net in earned income before it reduces your Social Security disability checks.) Life is good!

Let's say your portfolio has been doing well, providing a healthy income while continuing to grow in value, but you need a larger lump of cash for a one-time unusual project (such as building a workshop/observatory). Do not just take the money distributed across all your mutual funds like you do for your monthly income.

Look for a mutual funds that has underperformed the rest. When you sell shares from it, the capital gains you will pay taxes on will be less than selling shares in your better performing mutual funds. At tax time, you will pay much less income tax on the capital gains.

In my case, FLSPX had only grown 62% over the last six years, so it is the dog. When it comes time to replace the Jaguar with a Corvette convertible, part of this dog will die. (I am glad my Springer spaniels do not read my blog.)

When you take a distribution after retirement age, you owe both federal and state income tax on it. You could take out a couple million and pay 35% in taxes. With that you can buy an estate in Wyoming, a nice house in Boise or Maui or a shabby townhouse in San Francisco. But the tax consequences are substantial. It is not like having several million in a savings account. You should have no problem borrowing money with that lump on your assets sheet but it is not quite as convenient as a huge savings account. You can move assets from one mutual fund to another without it being considered a distribution.

Suggestion: along with making the maximum contributions to a 401k or IRA, put taxed money (unlike your 401k contributions and employer matching funds which are not taxed at contribution, but at distribution) into a completely separate account. Buy aggressive mutual funds in that account. When you need a lump of cash at retirement age, sell some of those mutual funds. You will owe capital gains taxes, but not income taxes when you take that money out, and long term capital gains taxes are much lower than income taxes).

If you found this information helpful, feel free to make a donation. If you don't feel like making a donation, put what you learned above to work for a year, come on back--you may find yourself willing to make a somewhat larger donation!